.png/LyyCD80m7Jnw1yFNHw8rRiV8d6sgRWrvaL0K31WB.png)

Understanding the Debt Consolidation Loan

Related Posts

-

Understanding the Debt Co ...

-

By-General Manager

-

3 months ago

-

-

BUILDING YOUR FUTURE WITH ...

-

By-General Manager

-

3 months ago

-

-

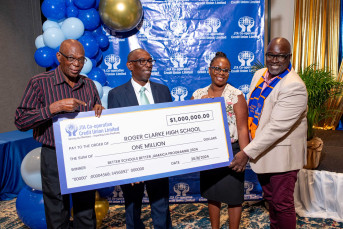

JTA Co-op Credit Union he ...

-

By-JTA Credit Union

-

3 months ago

-

-

Back-to-School Success St ...

-

By-Robert Ramsay, General Manager, JTA Credit Union

-

3 months ago

-

-

Happy Holidays from the J ...

-

By-Robert Ramsay

-

3 months ago

-

-

The JTA Co-op Credit Unio ...

-

By-Denise Walker

-

3 months ago

-

-

By-General Manager

-

3 months ago

Understanding the Debt Consolidation Loan

We are a member owned financial organization that serves teachers and other workers in the education sector who are members of the Jamaica Teachers’ Association. Since our establishment we have worked hard to ensure that our members are able to ‘BE THEIR BEST’.